Why decentralized wireless matters now

The telecommunications sector is undergoing a structural rupture. For decades, centralized telco monopolies have controlled the infrastructure, pricing, and access to connectivity. This model is fragile, capital-intensive, and increasingly resistant to the rapid innovation cycles demanded by 5G and future network generations. Decentralized Physical Infrastructure Networks (DePIN) offer a counter-model: community-owned infrastructure where participants are incentivized to build and maintain the network through token rewards rather than corporate equity.

The economic argument is stark. Traditional telco expansion requires massive upfront capital expenditure (CapEx) for tower construction and spectrum licensing. DePIN projects like Helium or similar wireless initiatives lower the barrier to entry, allowing individuals and small businesses to deploy nodes. This distributed approach not only accelerates coverage but also creates a more resilient network topology that is less susceptible to single points of failure. As noted by industry analysts, the sector’s strength lies in its ability to mobilize idle resources—spare bandwidth and unused hardware—into productive network capacity.

However, this shift carries significant risk. Regulatory uncertainty looms large. Governments are still grappling with how to classify token-based compensation models and whether decentralized nodes constitute regulated telecommunications infrastructure. Compliance costs could stifle growth, and legal challenges may force projects to adapt their economic models mid-stream. Investors must navigate a landscape where technological promise collides with evolving legal frameworks.

The market is already pricing in this potential. According to Messari, the DePIN market cap stood at over $50 billion in 2024 and is projected to reach up to $3.5 trillion by 2028. This explosive growth trajectory reflects investor confidence in the model’s ability to disrupt traditional telecom, but it also amplifies the stakes. Success depends not just on technology, but on the project’s ability to survive regulatory scrutiny and deliver reliability that matches centralized incumbents.

The race for decentralized 5G is not merely about technology; it is a battle for control over the physical layer of the internet. Those who can build a network that is both economically viable and legally compliant will define the next era of connectivity. The alternative is a fragmented, inefficient system where access remains a privilege of the few, controlled by legacy providers unwilling or unable to adapt.

Helium Mobile leads the 5G transition

Helium Mobile has emerged as the primary consumer-facing proof of concept for decentralized wireless infrastructure. While the broader DePIN sector grapples with scaling hardware, Helium has shifted focus to delivering actual 5G service to everyday users. This pivot from speculative mining to tangible utility marks a critical test for the entire industry's viability.

The network relies on a distributed model where users host hotspots to extend coverage. This approach reduces capital expenditure for carriers but introduces significant regulatory friction. The Federal Communications Commission (FCC) and international bodies are scrutinizing how token incentives interact with spectrum licensing. Helium must navigate these complex rules while maintaining service reliability that rivals traditional carriers.

Coverage growth remains the primary metric for investor confidence. The company has expanded its footprint across major metropolitan areas, leveraging the existing hotspot network to offer competitive data plans. However, the transition to true 5G speeds requires denser infrastructure than current 4G LTE deployments allow. The gap between promised coverage and actual user experience remains the central risk factor.

Market capitalization for Helium’s token reflects this tension between potential and execution. Investors are betting on the network’s ability to attract enough hosts to achieve critical mass. If regulatory hurdles stall expansion, the economic model could fracture. The coming year will determine whether decentralized 5G can sustain itself without perpetual subsidies.

The race is no longer just about building networks; it is about surviving the regulatory and technical realities of global telecommunications. Helium’s success or failure will likely dictate the trajectory for all subsequent DePIN wireless projects.

Niche players in mapping and IoT

Beyond the primary wireless giants, a secondary layer of DePIN projects is emerging that focuses on data density rather than raw signal coverage. These networks address the "last mile" of physical infrastructure by providing mapping precision, IoT sensor telemetry, or specialized compute verification. While they lack the immediate ubiquity of 5G-like protocols, they offer critical data layers that could become indispensable as decentralized networks mature.

The regulatory landscape for these niche players is particularly volatile. Because many rely on token incentives to recruit participants for data collection or sensor deployment, they face heightened scrutiny regarding securities laws and data privacy. Projects that cannot demonstrate clear utility beyond speculative token holding risk being shut down before achieving scale.

Helium (HNT) has pivoted from its original IoT focus to become the dominant force in mobile connectivity, yet its legacy IoT network remains a benchmark for decentralized sensor data. Theia (TIA), often confused with Celestia, is not a DePIN project; Celestia is a modular blockchain layer. The primary competitor in the IoT data space is often IOTA (IOTX) or similar sensor-focused networks, but for the purpose of this comparison, we look at the leading tokenized infrastructure assets that bridge connectivity and data.

The following table compares the utility, network status, and primary use case of three major infrastructure tokens, highlighting the divergence between pure connectivity and data-centric models.

| Token | Token Utility | Network Status | Primary Use Case |

|---|---|---|---|

| HNT | Governance, staking, and paying for mobile/IoT services | Mainnet active with growing mobile coverage | Decentralized 5G and IoT sensor data |

| TIA | Governance of the Celestia modular blockchain | Mainnet live, high TVL in rollups | Data availability for modular blockchains (not direct IoT) |

| IOTX | Staking for node operators and paying for device services | Mainnet active with global IoT partnerships | IoT device identity and data telemetry |

Technical Viability and Network Stability

DePIN wireless networks face a steep engineering challenge: matching the latency and throughput of legacy telco infrastructure. While the market cap for DePIN has surged past $50 billion, projecting toward $3.5 trillion by 2028, the underlying network reliability remains unproven at scale. Decentralized nodes must prove they can deliver consistent service quality without the centralized control mechanisms that traditional carriers use to manage congestion and interference.

Latency is the primary point of failure for decentralized wireless. In legacy 5G, network slicing and centralized baseband units allow operators to prioritize traffic and minimize lag. DePIN relies on distributed hardware, often consumer-grade routers, which introduces variable ping times and packet loss. For applications like autonomous vehicles or real-time industrial control, even a 10-millisecond delay can render the network useless. The current generation of DePIN wireless protocols struggles to guarantee the sub-10ms latency required for true 5G performance.

Proof-of-coverage mechanisms attempt to solve this by incentivizing nodes to provide genuine signal rather than just token rewards. However, these systems are vulnerable to gaming and spoofing. Nodes can artificially inflate their coverage reports, leading to a false sense of network density. This regulatory and technical uncertainty creates a high-risk environment where investors and enterprises must weigh the potential for lower infrastructure costs against the reality of inconsistent service delivery.

The technical gap between DePIN and traditional carriers is narrowing, but it remains significant. As the sector matures, the focus will shift from tokenomics to engineering rigor. Networks that fail to solve the latency and stability issues will likely remain niche experiments, while those that achieve telco-grade performance could disrupt the market. Until then, the risk of network unreliability remains a critical barrier to widespread adoption.

Regulatory hurdles and token economics

DePIN wireless projects face a dual threat: regulatory classification and economic fragility. While the sector’s market cap surpassed $50 billion in 2024, projecting toward $3.5 trillion by 2028, this growth masks deep structural risks. Investors are navigating a landscape where token utility is often indistinguishable from unregistered securities, and spectrum access remains tightly controlled by legacy incumbents.

The Federal Communications Commission (FCC) treats wireless spectrum as a public trust, not a commodity for decentralized speculation. Projects like Helium have already faced significant legal friction over spectrum interference and licensing. As DePIN networks scale, the FCC is likely to enforce stricter compliance on frequency usage, potentially invalidating the core value proposition of permissionless wireless nodes. Regulatory uncertainty regarding token compensation models requires careful navigation, as these networks expand globally.

Beyond spectrum, the sustainability of incentive models is questionable. Most DePIN projects rely on token emissions to attract hardware providers, creating a Ponzi-like dynamic where new user growth must outpace token inflation. If regulatory bodies classify these tokens as securities, liquidity could evaporate overnight. The reliability of decentralized services must match centralized providers, but current tokenomics often prioritize speculation over network stability.

The convergence of these factors creates a high-stakes environment. Projects that fail to secure clear regulatory frameworks or develop sustainable, non-inflationary token economies may collapse under the weight of compliance costs and investor skepticism. The race for decentralized 5G is not just technological; it is a legal battle for survival.

Evaluate DePIN Wireless Viability

DePIN wireless investments operate in a high-stakes environment where regulatory uncertainty and technical reliability define success. Before allocating capital, you must verify that a project’s decentralized services can match the uptime and user experience of established centralized providers. The market cap for the broader DePIN sector exceeded $50 billion in 2024, but individual project viability varies wildly based on execution and compliance.

Check on-chain metrics for active node distribution and real-world hardware deployment. Avoid projects with inflated token counts but sparse physical infrastructure. Use the

to gauge overall market liquidity, which often correlates with project stability.

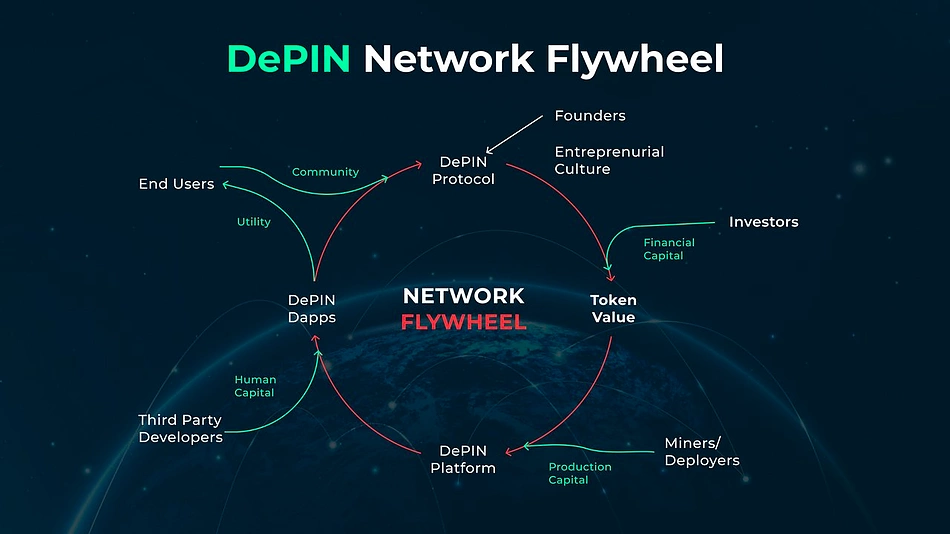

Ensure the token has a clear purpose beyond speculation. It should facilitate payments for bandwidth, storage, or compute resources within the network. Projects lacking a functional flywheel between hardware contribution and token reward are high-risk.

Regulatory frameworks for token compensation models are still evolving globally. Prioritize projects that have engaged with legal experts to structure their incentive models in compliance with securities laws. Non-compliance poses an existential threat to any DePIN venture.

The intersection of physical infrastructure and digital finance requires rigorous due diligence. Treat every investment as a bet on both engineering capability and legal resilience.

DePIN Wireless FAQs

The race to decentralize 5G infrastructure is accelerating, but it carries significant regulatory and operational risks. As DePIN wireless networks scale, participants must navigate complex tokenomics and compliance landscapes.

No comments yet. Be the first to share your thoughts!